When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

I think it's important to tell LV and the garage that if it is written off then you want the option to buy back. If not you may find that the garage will just scrap it out. With LV you can start by asking what the options are if it is not commercially viable to repair but the garage I suspect you must tell in no uncertain terms you're exploring this option. Perhaps ask them for an estimate to repair to non insurance standards or if you supply parts.

The whole process is annoying as the insurer will instruct the repair shop where to buy parts, at what cost, what kick back they will want from the repairer and even so the same shop would do just as good a job for you for much less. So the car may get the Cat N status when the insurance repair is uneconomic but the same shop would do just as good a job for you for far less meaning it's not uneconomic. I have quite a lot of sympathy for body shops that rely on insurance work, their margins are not great and the standards expected are high. Often inappropriately high.

Well I would say that you own the car and they cannot take it away and scrap it its all your decision what happens .

Problem is its all down to the ���

I thought that once you make a claim on insurance then the process starts and you have to mitigate their losses and if they decide it's uneconomic to repair then that's it. You either accept a negotiated settlement and it becomes their car which they may (probably will) sell back to you or you withdraw the claim and you get nothing but you do keep the car. I may be wrong though. It certainly seems to be the way it works.

Why would you buy back your own car ? It looks like �200 worth of parts on ebay all bolted on then a respray of the front if you cannot get the right coloured panels. If they are going to offer you say �8000 and you buy it back for less say �6000 then you are in with a chance even if its N classified. Take it to a body shop when its done for them to certify its ok. I am sure you can find a bent back street place. Makes you wonder if fully comprehensive is worth the money

Last edited by Pistnbroke; Dec 2, 2021 at 02:42 AM.

Yes, my insurers (LV) have (so far) admitted liability - the car was actually recovered to one of their approved body shops this morning.

Now is when it gets complex. Insurers have to repair the damage to "as good as new" status that means using genuine OEM parts. They will then assess how much it will costs to repair as a percentage (approx 60%) of the current value. That value is the current trade price. In many of these situations as per drmike's earlier post they will deem it not economically viable to repair to these exacting standards or it may not be possible to as parts are not available. They can then declare it a category N write off or if unroadworthy a category A or S write off (https://www.carwow.co.uk/guides/choo...c-or-cat-d-car and https://www.car.co.uk/media/guides/i...category-n-car).

I suspect they will declare this a category N write off as original body panels etc are no longer available. However, the guy who collected the car today did say my insurer occasionally sanctions using old parts in which case there are several candidates on eBay for �200 ish.

If they don't go for this and offer me cash then I have the option to buy it back and get another body shop to fix at my expense - annoyingly the guy who usually does these jobs for me is away until after Christmas .

You can tell I've been researching this.

Anyway, will find out in a day or 2.

Steve

If they declare it a CAT N and you buy it back do they also pay the value of the car or are you left with bugger all? Either way it seems like a cop out to me. You spend all the money over the years on insurance only for them to say it's not worth their time.

My understanding is that in the UK the insurer must restore you to the position you were in before the claim. If they can repair then it must be done to a high standard which will be expensive but will make the car as good as it was before the claim. If they feel they cannot do that without exceeding the cost of replacing the car (or in fact I think around 75% of the value of the car) then they write it off and give you the money to allow you replace the car with something equivalent and there's where you can negotiate a bigger settlement.

I don't think you can say I can get a cheap repair so give me the money to do this. I believe this is because it opens a can of worms over warranties etc. The insurer will want to be satisfied that they have fulfilled their obligation to restore you to the state you were in before the claim with a full warranty and of course that costs money, more than you'd have to pay.

Maybe I'm wrong, let's hope so. It will be detailed in the T&C of your policy but a rather dull read!

EDIT: I think I may in fact be wrong and they have the option to give you some money just to go away and settle the claim. In my documents that's listed as an option but then they don't expand on it. This would almost certainly be your best outcome as I imagine it takes almost nothing to reach 60% of the value of the car using manufacturer's parts and labour. I'd still be declaring an interest in buying back should they go the Cat N route.

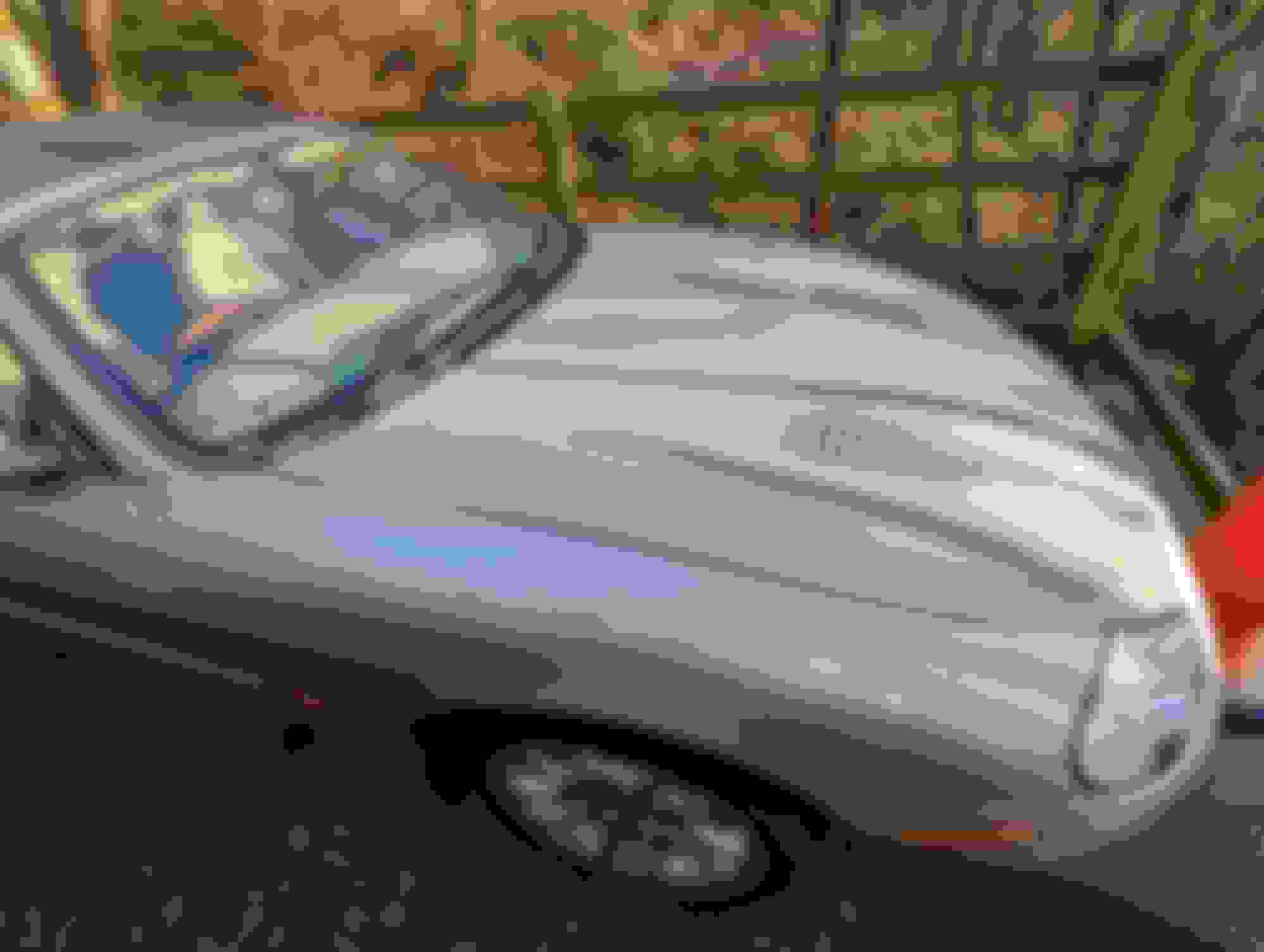

So just spoke with body shop and they have been given the green light by LV to repair.

Body shop manager said they have ordered new wing and bonnet from Jaguar who gave a price so he's pretty confident they can actually source new panels.

Interestingly the body shop manager said something pretty similar - never sure how much these "old cars" are worth until you dig deeper. Given that he was initially quoted something like �1500 for a new bonnet by JLR I'm guessing the resale value is higher than expected. So far it's kudos to LV for agreeing and I'll be looking to move my other cars to them on renewal - the Discovery Sport is already with them. However, there is still a lot than go wrong so until it's back on my drive all fixed I'm keeping fingers crossed.

Steve

I'm with LV - added the XKR to my existing policy, they gave me the same 10 year max discount, so was well happy - 2 cars for less than �350 a year

Just checked my policy, and they've got the value at �7500 - I paid �13,500 for it and so far it owes me about �16k, which is slightly less than I'd expect to pay for one if I was buying in the spring

Makes you wonder what the correct value is? What someone would be willing to pay, I suppose.

Doubt I'd get an XKR convertible, 2004, less than 100k on the clock, new front end suspension and bushings, bodywork cut-out and welded with a complete respray for under �20k? Especially with Recarro, Brembo, 20" refurbished Montreals with original spec Dunlops, loads of tread all round ,and all the extras that were on it as originally which made it, I've been told, OTR price of about �72k when new

Suppose these cars are worth more as spares if anything goes wrong